I was asked this question during an interview, and I couldn't answer it. Well I have researched it and here is the answer.

The context is

how would we track a bitcoin's transaction to see if a wallet is a money launderer?

Below is taken from ethereum design rational.

Bitcoin

- Bitcoin balance are tracked by unspent transaction outputs (UTXO), think each UTXO as a coins like nickle, penny, dimes.

- each

UTXO coinhas to have a value, and an owner.- this has a high degree of privacy, users can use a new address for each transaction they receive, and will be difficult to link to each other.

- A user's balance in the system is the total value of the set of coins for which the user has a private key capable of producing a valid signature

- Bitcoin Blockchain has limit of 1MB. so there is a finite # of transaction to fit in a block.

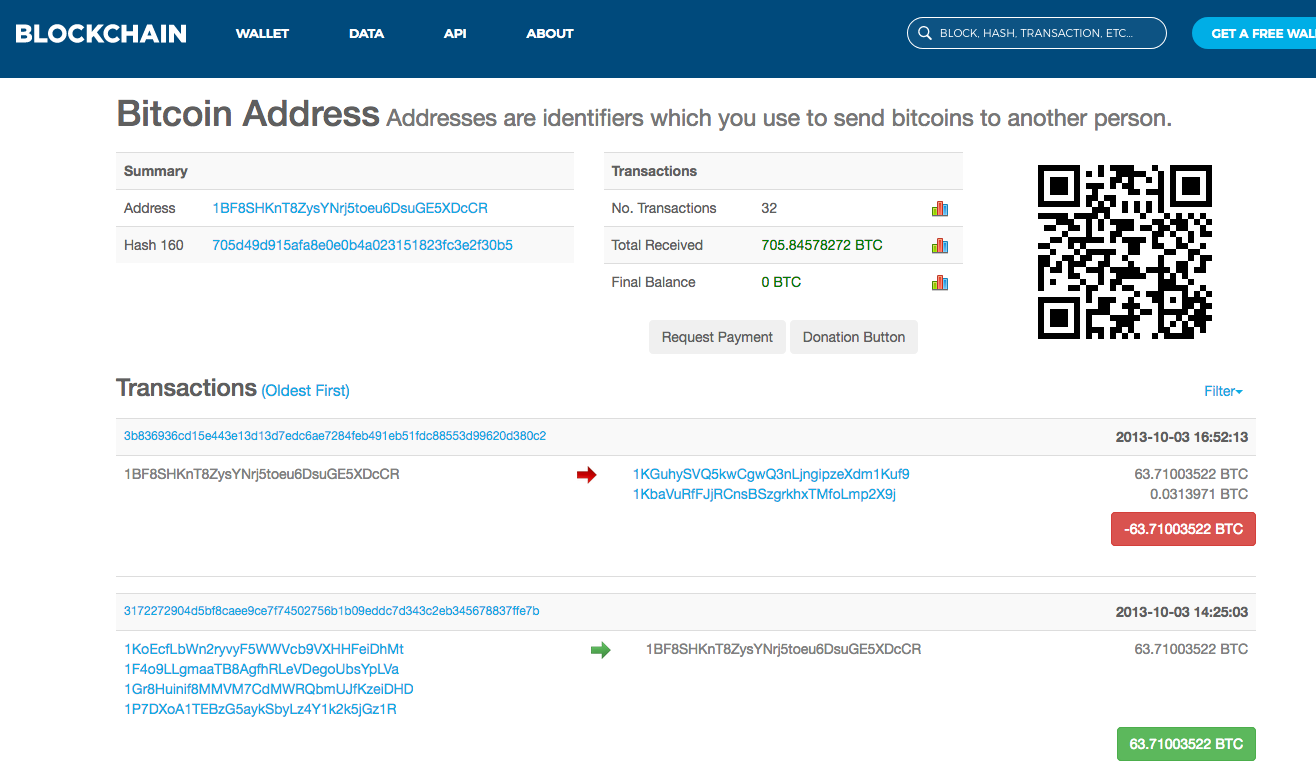

on blockchain.com, we see that every wallet's transaction is recorded publicaly.

Ethereum

- Ethereum the global state stores a list of accounts, with balance, codes and internal storage.

- the balance is represented by a

uintnumber.- this means ethereum tokens are more

fungible.

- this means ethereum tokens are more

- Ethereum blockchain has no blocklimit, # of transaction in a block is decided by the miner.